Australia

Australia

USA

USA Canada

Canada UK

UK Ireland

IrelandIs your mortgage application rejected multiple times? There are many people in the same situation as you.

An increasing number of mortgage applications in Australia are being turned down, usually because the borrowers were not well prepared. Though getting a home loan feels simple, lenders look at various factors, and mistakes can cause your loan request to be rejected.

There are various factors, like a poor credit report or unstable earnings, that can stop you from being approved. The good point here is that if you’re aware of these typical traps and get ready beforehand, your odds increase a lot. This blog explains why some mortgage applications get refused and gives useful tips on how to get your mortgage approval.

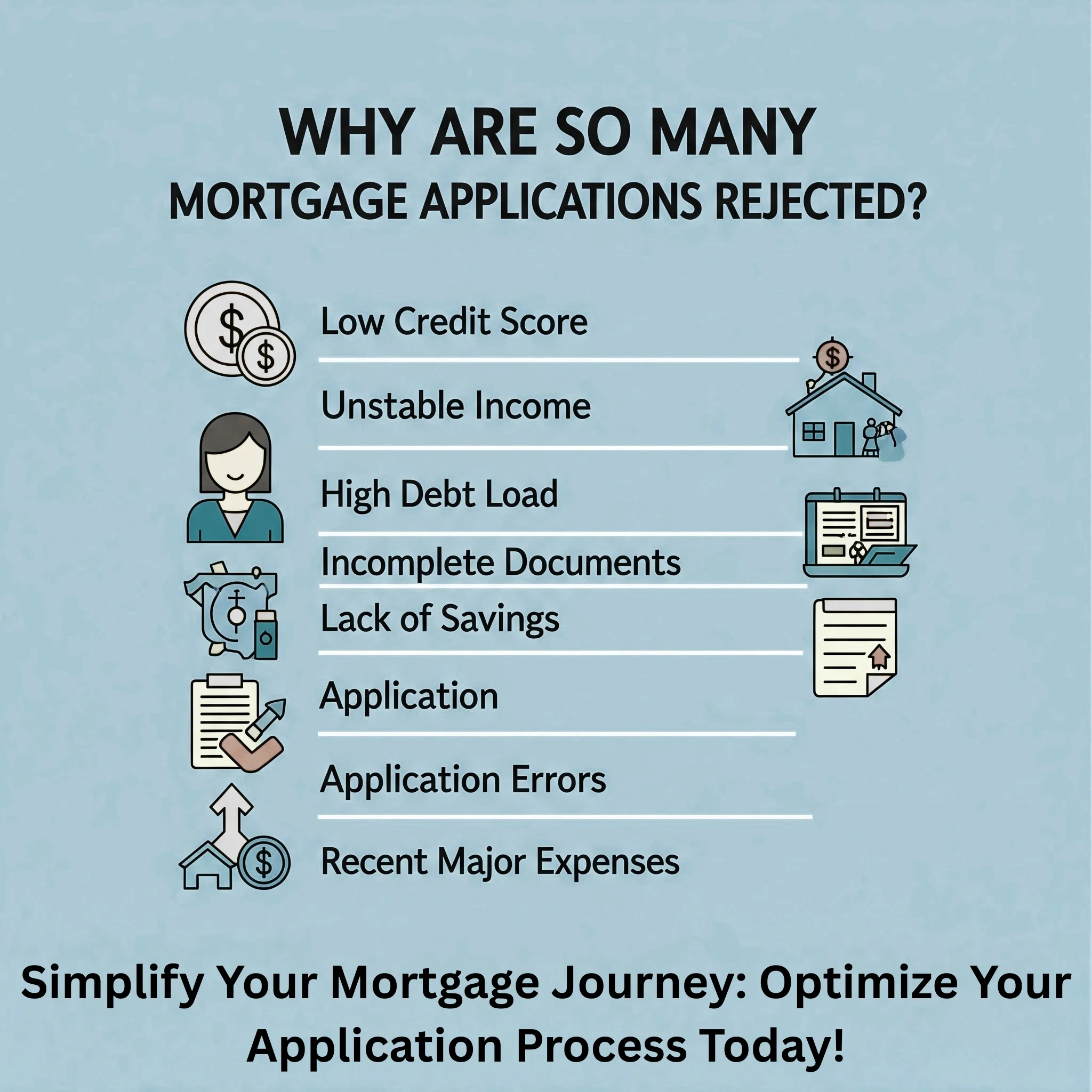

Why Are So Many Mortgage Applications Rejected?

Approximately 40% of home loan applications are being declined, highlighting the challenges many face in securing a loan. Apart from having resources and selecting a good lender, being financially responsible and presenting all needed documentation are important when applying for a mortgage. It’s useful to explore the main factors that cause mortgages to get rejected in Australia.

A History of Unpaid Debts

Before anything else, lenders will check a borrower’s credit history while processing a mortgage application. Past actions towards paying off debt, such as loans, credit cards, utilities and miscellaneous bills, appear on your credit report. When applicants show overdue payments, defaults or apply for more credit than needed, lenders believe they are not responsible with their finances.

A late repayment can drop your score and suggest you may be risky to lenders. The credit policies of Australian lenders are strict, so many of them reject your application just for borderline scores. Lenders are more confident in you when your credit history shows many on-time and careful payments are made.

Unstable Employment

Employment can show if you handle money responsibly over the years. Mortgage lenders require proof that the income you make will last long-term. If in the past couple of years you have changed jobs, are your bosses with different income or have jobs that don’t last or provide consistent records, it could cause issues with lenders.

In addition, employers may see someone employed for less than six months as too great a risk, especially if this is part of a probation period. Similarly, if you’ve been working continuously in the same industry, it means you are more likely to have a regular and predictable income, which makes it easier to get your mortgage approval. Loan providers look for people who have had dependable earnings for at least six to twelve months.

Enormous Debt-to-Income Ratio

You might not be able to apply for a loan if you carry multiple debts, even if your income is good. A lender factors your debt-to-income ratio to discover how much you spend on paying off current debts every month. When you have car loans, credit cards, personal loans or use buy-now-pay-later and you earn less than with a mortgage, lenders may decide the loan is too risky due to your expenses.

Having a high debt ratio could suggest that you might have trouble meeting new debt payments without stress. You should pay off as much debt as you are able before applying for a mortgage process to show you can handle more financial obligations.

Missing or Incorrect Documentation

Providing the correct documents is very important in the entire process of applying for a mortgage loan process. The lender will check your name, social security number, income, assets, debts and your savings records. Sometimes, delays or rejections happen to applications because the required documents are not provided correctly.

Examples are: out-of-date payslips, bank statements differing from what a person claimed or mistakes in the stated expenses. Whenever you have a different amount, this may make people question your honesty. Entering the wrong start date at work or missing a signature on a form can lead to complications. An application that is prepared carefully and is accurate helps to build trust and get the approval faster.

Insufficient Genuine Savings

Lenders are more interested in the process of saving your money than just seeing your total savings. Genuine savings means money you’ve built up little by little through a period of at least three months. It reveals that you stick to your budget and can keep up with your loan repayments.

If your down payment include infrequent gifts, windfalls or loans, lenders might not consider you ready to maintain a mortgage. Posting regular fresh savings to your account shows the bank you’re financially responsible and assists your mortgage application.

Understanding Each Stage of Your Mortgage Application

Taking the steps in a mortgage loan process one-by-one can simplify everything. If you’re a first-time homebuyer or a broker, learning what is going to happen at every stage gives you confidence and lowers the chance of making mistakes.

-

Doing a Financial Assessment at the Start: Borrowers check their credit score, see how much they owe and look at how much they have saved. You should now determine your budget and find out how much you are able to borrow.

-

Loan Pre-Approval: A pre-approval from a lender will show you are genuine and demonstrate your borrowing power. It helps you see possible problems before you look for a home.

-

Property Search and Make an Offer: After getting pre-approved, buyers start looking for properties they can afford using their loan amount. When the property that fits your needs is located, you can make an offer which generally depends on getting a final approval of your mortgage.

-

Complete Mortgage Application Form: It requires preparing and submitting a mortgage application form, together with income proofs, bank statements and property information.

-

Reviewing Loan Terms by the Lender: After receiving the application, the lender analyzes it, checks if it’s risky, looks over the paperwork and possibly gets a property appraisal. If everything proceeds smoothly, the organization gets either conditional or full approval.

Disbursing Settlements and Loans: Post-approval, the contracts are signed and the settlement begins. The lender gives the funds and the buyer officially becomes the owner.

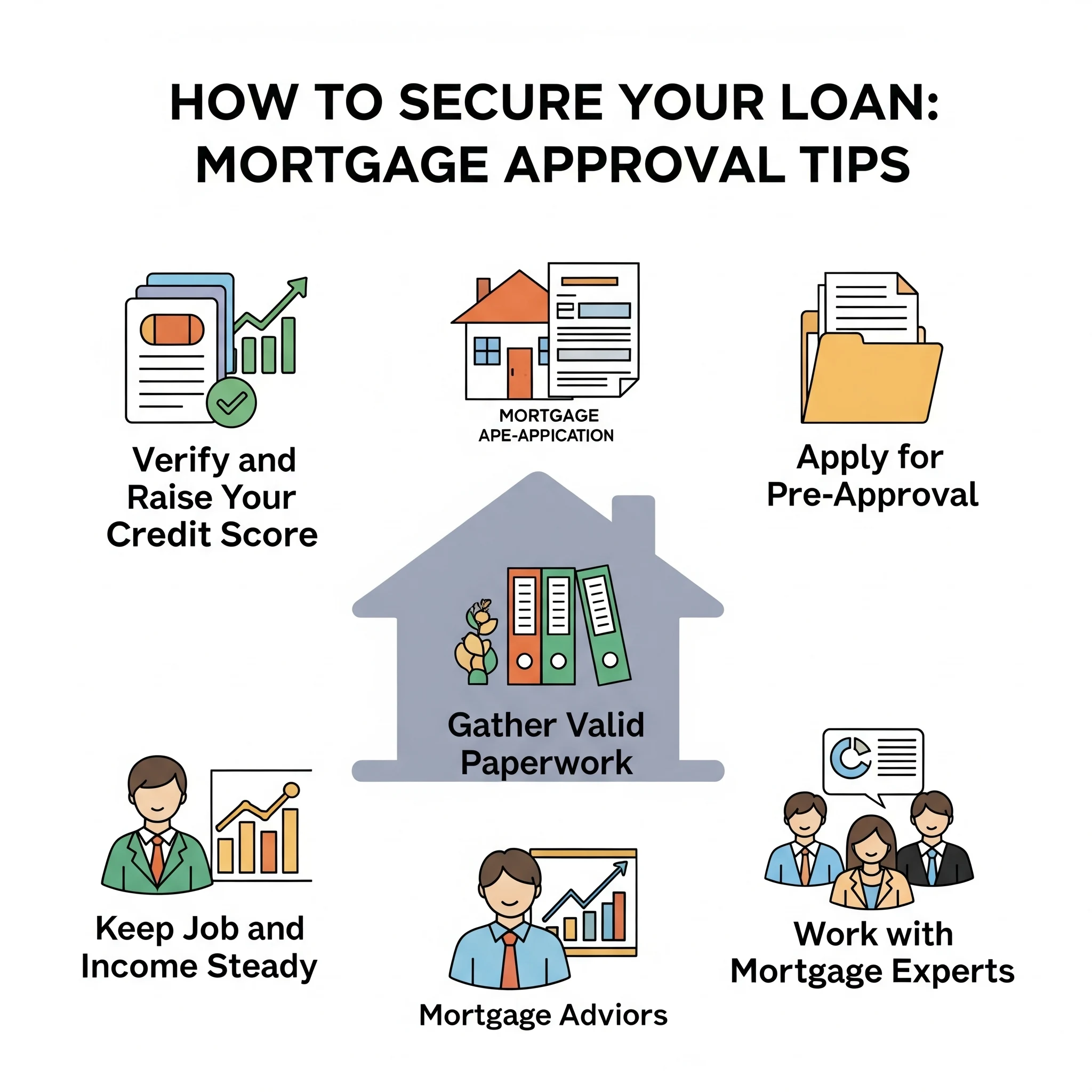

How to Secure Your Loan: Mortgage Approval Tips

Getting mortgage approval can be clearer than you expect. Follow a few mortgage approval tips and ensure you are well-prepared, and it will be much easier to get approved for a home loan. Here are some tips that help applicants make a more compelling application and dodge common lender issues.

Getting mortgage approval can be clearer than you expect. Follow a few mortgage approval tips and ensure you are well-prepared, and it will be much easier to get approved for a home loan. Here are some tips that help applicants make a more compelling application and dodge common lender issues.

✅ Verify and Raise Your Credit Score

Look at your credit report well before applying for a formal mortgage process, so you have an awareness of your situation. You may get a free credit file from agencies like Equifax or Experian. Look for any mistakes, unpaid bills or old information that may affect your score. If you see that you have more credit card debt than you can pay, try to settle those debts as soon as you can.

Taking out a new loan or credit card just before applying for a mortgage should be avoided. They often understand multiple credit applications to mean the borrower is feeling a financial crunch. Looking after your credit score is usually the surest proof of your ability to handle a mortgage financing process properly.

✅Apply for Pre-Approval before House Hopping

Getting pre-approved for a loan gives you a big head start over other buyers. It helps you real amount you can afford and shows real estate agents and sellers you’re really interested in buying. Most importantly, it finds any weaknesses in your finances early on, so you still have time to fix them before the full application.

Getting pre-approved helps you avoid looking at houses that are too expensive for you. Keep in mind that your approval is usually only good for a short time (typically 3–6 months), so you need to act quickly.

✅ Gather and Confirm the Validity of Your Paperwork

Mortgage loan applications process depend heavily on your documentation. With proper and well-organised documentation, everything will work out more easily for you. You will be required to show payslips, tax returns, bank statements, ID documents and evidence of financial obligations. The information is used by lenders to evaluate how much you earn, what you spend and your general financial well-being.

Missing or unclear documents can cause the process to be delayed or ruined. Before the last minute, go through your documents to confirm they are correct and still current. A properly prepared file makes decisions from the lender faster and makes a good impression.

✅Keep Your Job and Income Steady

Being stable in your job is very ,important to lenders. Employment changes you go through during the mortgage process such as moving to another job, switching to part-time hours or starting an enterprise, may raise concerns. Shifting jobs or role,s even if your income doesn’t change or goes ,up can affect your lender’s evaluation of yourfor financial situation. You should continue at your job until you get the loan approval as long as possible.

For self-employed people, being able to present at least two years of tax returns and financial documents is necessary. Lenders will require evidence that your income is constant so you can pay back your loan each month.

✅Working with Mortgage Experts or Brokers

Trying to do a mortgage application without help can be very confusing, as many lenders are offering various things, and e,ach has unique requirements. It is at this stage that working with a finance expert such as a mortgage broker, becomes especially useful. A broker will check your finances, suggest the best lenders for you and assist in completing a good application. They can talk about challenging situations, perhaps related to your work or financial history, to help your case get approved. Following their advice often helps you avoid being rejected unnecessarily and saves you time and money by giving you a chance to select from a wider range of loans.

How Can Aone Outsourcing Make Your Mortgage Approval Easier?

We help simplify how brokers, aggregators and financial institutions in Australia work with mortgages. It is clear to us that mortgage approval takes a lot of effort, and even a little delay or error may influence your business and how pleased your clients are.

This is why every part of the mortgage loan process we work on is optimised for speed, accuracy and adhering to compliance rules. We offer you:

-

✅ Reviewing and organising the paperwork needed by the lender to avoid any mistakes.

-

✅ Up-to-date data entry ensures there are fewer errors, and the application speeds up.

-

✅ Tailored compliance checks focused on the rules your lenders use – so you stay in line with all requirements.

-

✅ Managing and following through with your application, from initial steps until the closing.

-

✅ Ability to scale support in the back office, keeping up with your company activities.

If you are dealing with these mortgage applications every day, Aone can help you streamline your operations, reduce rejections and give clients a better experience.

Wrapping Up!

It isn’t hard to get through mortgage approval if you are guided along the way. To avoid the usual problems, include bettering your credit score, fixing your financial status, assembling correct documents and talking with someone experienced before you try to be approved for a mortgage application.

Managing all these applications at once, while keeping the work compliant and at the expected standard, is the biggest concern for both brokers and mortgage firms. For this reason, our team exists.

To speed up your mortgage processes, reduce wait times for clients and provide a better experience, you can count on Aone Outsourcing.

Let’s partner to make your business better. Contact Us Today!!